Master these fundamentals to protect your business:

- Cash flow measures timing of money movement, not just profit. A profitable business can still fail if cash runs out.

- Monthly forecasting (even simple projections) helps you spot problems 30 days before they become crises.

- Warning signs like shrinking reserves or slower customer payments signal trouble early when you're still in control.

- Small, consistent habits beat complex spreadsheets. A 15-minute weekly review can prevent major cash emergencies.

You made payroll last week, but this week's vendor invoices are due and your biggest client still hasn't paid. The profit-and-loss statement says you're doing fine, but your checking account tells a different story.

It's the 2 a.m. wake-up call. The mental gymnastics of deciding which vendor to pay first. The personal credit card you used to cover payroll because the business account came up short. According to SCORE, cash flow problems rank among the top reasons small businesses struggle or close their doors entirely.1

These moments aren't signs of failure. They're signals that your cash flow system needs attention. Here's the good news: managing cash flow isn't about becoming a financial expert or mastering complicated formulas. It's about building simple, repeatable habits that give you visibility into what's coming and control over your decisions. This guide breaks down the basics every owner needs, using real examples and practical steps you can start using today.

Why cash flow is the #1 predictor of survival

Profit is a measure of success. Cash flow is a measure of survival.

Imagine you run a small manufacturing business and land a $10,000 order. Your costs are $6,000, so you'll earn $4,000 in profit. Sounds great, right? But here's the reality: you pay $6,000 up front for materials and labor today. The customer pays you $10,000 in 60 days.

On paper, you're a success. In reality, you're a bank for your biggest customer.

For two months, you're $6,000 short, even though you "made money" on the deal. That two-month gap is where businesses fail, not because they aren't profitable, but because they run out of cash to operate. That timing gap is cash flow. It's the difference between the money coming in and the money going out, measured day by day. If you can't cover payroll, rent, or supplier invoices during that gap, profit doesn't matter. The business stops.

This isn't about revenue size. A company with $2 million in annual sales can fail because of poor cash timing. A smaller operation with $500,000 in revenue can thrive because the owner understands when money actually arrives and plans accordingly. Survival depends on having cash available when obligations come due, not on how impressive your year-end numbers look.

What cash flow really means (more than profit)

Cash flow tracks the actual movement of money: what comes in (inflows), what goes out (outflows), and the timing of both. Working capital, the cushion between your current assets and current liabilities, determines how much room you have to operate when timing doesn't line up perfectly.

Different industries face different pressure points:

Restaurants see high daily inflows from customer payments, but margins are thin and costs hit constantly. Food spoilage, hourly wages, and utility bills create steady outflows. A few slow nights can tighten cash quickly, even when monthly revenue looks healthy.

Healthcare practices often wait 30 to 90 days for insurance reimbursements, even though they pay staff, rent, and suppliers on normal schedules. The gap between delivering care and receiving payment creates persistent tension, requiring careful planning and adequate reserves.

Manufacturing businesses pay for raw materials and labor weeks or months before finished products ship and customers pay invoices. Long production cycles mean significant cash goes out the door long before any comes back in, making working capital management essential.

Service businesses like plumbers, electricians, and HVAC contractors traditionally invoiced clients and waited for checks by mail. Today, many use electronic invoicing with text-to-pay links or mobile payment devices that let field technicians accept payment at the time of service. This dramatically increases the speed to payment and reduces the risk of carrying cash or checks.

Understanding your industry's specific rhythm matters. The timing patterns that work for a retail shop won't match a consulting firm's needs. Knowing when your inflows typically arrive and when your outflows hit helps you plan for gaps instead of scrambling when they appear.

Common cash flow problems for SMBs

Most cash flow problems fall into a few familiar categories:

Late-paying customers are the most common culprit. When invoices sit unpaid for 45, 60, or 90 days, you're essentially providing free financing to your clients while still covering your own costs on time.

Seasonal fluctuations hit businesses in cycles. Landscapers earn most of their revenue in spring and summer but face expenses year-round. Retailers see spikes during holidays but slower months in between. Without planning, the slow periods drain reserves built during busy times.

Inventory swings tie up cash in products sitting on shelves or in warehouses. Ordering too much means money you can't use for other needs. Ordering too little means lost sales. Finding the right balance requires understanding your sales patterns and lead times.

Rising costs for materials, labor, or rent shrink margins and create pressure even when revenue stays steady. If your prices don't adjust quickly enough, the gap between what you earn and what you spend narrows, leaving less cushion for unexpected expenses.

Owner reality

You're not alone in this. These problems aren't just numbers on a spreadsheet. They show up in your life in specific, disruptive ways.

Late-paying customers might mean you're skipping your own paycheck to cover payroll. Seasonal fluctuations might mean delaying that critical hire because you need to preserve cash for the slow months. Inventory decisions might mean lying awake wondering if you ordered too much and tied up money you'll need for rent, or ordered too little and you'll lose sales. Rising costs might mean using your personal credit card to bridge a gap that shouldn't exist.

You work 60-hour weeks. You're generating revenue. On paper, the business is profitable. But the timing doesn't match up. Your customers pay in 45 days. Your suppliers want payment in 30. Payroll hits every two weeks like clockwork. The math works on an annual basis, but monthly? Weekly? That's where the stress lives.

These aren't signs you're doing something wrong. They're signals that your cash flow system needs structure. Most owners bootstrap their way through the early years without formal cash management processes. What works when you have two employees and five clients breaks down when you scale. The good news? Addressing these patterns early prevents bigger problems down the road.

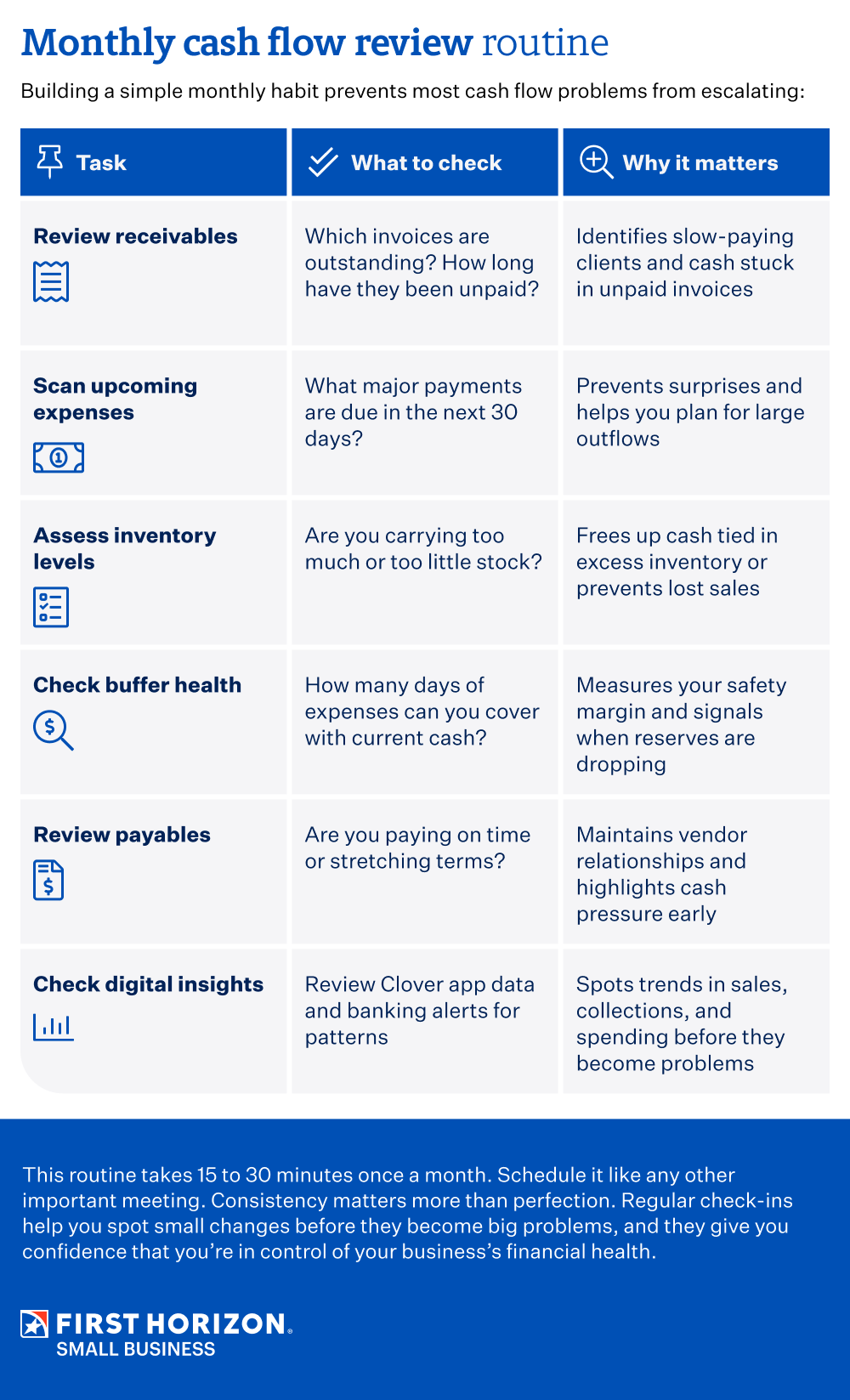

Simple monthly cash flow forecasting

Forecasting doesn't require complex models. A basic 30-day projection gives you enough visibility to make better decisions and avoid surprises.

Step 1: List expected inflows. Write down every payment you expect to receive in the next 30 days. Include customer invoices, recurring revenue, and any other money coming in. Be realistic about timing. If clients typically pay in 45 days, don't assume 30.

Step 2: List expected outflows. Document every expense you know is coming: payroll, rent, supplier invoices, loan payments, utilities, insurance, and taxes. Include both fixed costs (same every month) and variable costs (change based on activity).

Step 3: Separate critical from flexible expenses. This isn't just a list. It's your playbook for tough times. Critical expenses can't be delayed without serious consequences: payroll, rent, loan payments, essential suppliers. Flexible expenses can be adjusted or postponed if cash gets tight: new equipment, marketing campaigns, optional inventory. Knowing the difference gives you control when cash gets tight and options when you need them most.

Step 4: Calculate your projected balance. Start with your current cash balance. Add expected inflows. Subtract expected outflows. The result shows where you'll likely stand in 30 days. If the number is uncomfortably low, you have time to adjust now rather than react later.

Technology makes this easier. Tools like QuickBooks and FreshBooks automate much of the tracking. If you use Clover point-of-sale systems, the Clover App Marketplace offers apps that track sales patterns, automate invoicing, and accelerate payments. Many First Horizon Bank business clients integrate these tools with their business checking accounts to get real-time visibility into cash movement without manual spreadsheet updates.

The goal is awareness, not perfection. Knowing what's coming lets you make proactive decisions instead of reactive ones.

Signs your business may face a cash crunch

Early warning signs give you time to adjust before a cash problem becomes a crisis:

Shrinking reserves mean your cushion is disappearing. If your account balance trends downward month after month, even slightly, you're heading toward trouble.

Slower receivables show up when customers take longer to pay. If your average collection period stretches from 30 days to 45, then 60, cash is getting stuck in unpaid invoices.

Growing payables signal that you're delaying payments to suppliers or vendors. Stretching payment terms might buy time, but it also damages relationships and can lead to stricter terms or lost credit.

Increased short-term borrowing to cover routine expenses means your normal operations aren't generating enough cash. Relying on credit cards or lines of credit for everyday costs is a red flag.

Payroll pressure appears when you're cutting timing close or juggling accounts to make payroll. If covering your team's paychecks feels uncertain, cash flow needs immediate attention.

Catching these signs early gives you options: adjusting pricing, tightening collections, cutting discretionary spending, and having a conversation with your banker about cash management solutions before the situation becomes urgent.

Cash flow red flags

Some indicators signal more serious problems that require immediate action:

Using personal funds repeatedly to cover business expenses means the business isn't sustaining itself. Occasional owner contributions are normal in startups, but chronic dependence on personal money indicates a structural problem.

Past-due taxes create compounding issues. Tax obligations don't disappear, and penalties add up quickly. If you're delaying tax payments to cover other expenses, you're borrowing from a creditor that doesn't negotiate.

Maxed credit lines eliminate your safety net. Once you've used all available credit, you have no buffer for unexpected expenses or opportunities.

Vendor threats or service cuts mean relationships have deteriorated to the point where suppliers won't extend more credit or continue service. This limits your ability to operate normally.

"The first thing I ask a business owner is, 'What's your average collection period?' If they don't know, that's where we start," says Tim Harris, Business Banking Manager at First Horizon. "It's often the single biggest lever they can pull to improve their cash position without increasing sales. When owners come in early, when they first notice patterns changing, we have time to explore solutions that fit their situation. We'd rather help you plan ahead than watch you struggle through a crisis that could have been prevented."

If you're seeing multiple red flags, don't wait. Reach out to your banker, accountant, or a trusted advisor. The earlier you address serious cash flow problems, the more options you have.

Common questions about cash flow

How do I fix cash flow fast?

Start with receivables. Contact customers with overdue invoices and request immediate payment. Offer small discounts for early payment on current invoices. Delay non-essential purchases and negotiate extended terms with flexible vendors. These steps can free up cash within days or weeks.

What is a good cash flow margin?

A healthy business maintains enough cash to cover 30 to 90 days of operating expenses. The exact number depends on your industry and revenue stability. Seasonal businesses need larger buffers. Service businesses with steady monthly revenue can operate with smaller cushions.

How often should I review cash flow?

Monthly reviews work for most stable businesses. Weekly check-ins help during growth periods, seasonal peaks, or when you're managing through challenges. The key is consistency and catching changes early.

Can a profitable business have cash flow problems?

Absolutely. Profit measures revenue minus expenses over time. Cash flow measures actual money available right now. A business can show profit on paper while waiting for customer payments, creating a cash shortage that threatens operations.

What tools help manage cash flow?

Accounting software like QuickBooks or FreshBooks automates tracking. Point-of-sale systems like Clover provide real-time sales data and access to over 500 apps through the Clover App Marketplace that can help with invoicing, appointment scheduling, inventory tracking, and payment acceleration. Banking platforms offer alerts and reporting. For more guidance, the SBA's cash flow resources and SCORE's financial templates provide free planning tools. First Horizon's cash management solutions integrate many of these capabilities.

From survival to stability, from stability to growth

Cash flow management builds habits that give you visibility and control. When you know what's coming, you make better decisions. When you spot problems early, you have time to fix them before they threaten your business.

The difference between reacting to cash emergencies and planning proactively is often just a simple monthly routine and the willingness to pay attention to patterns. Small, consistent actions compound over time, creating stability that lets you focus on growth instead of survival.

Mastering your cash flow isn't just about avoiding crises. It's about building a resilient business that can seize opportunities, invest in growth, and give you the freedom to lead, not just manage.

If you're ready to strengthen your cash flow foundation or want to talk through your specific situation, First Horizon bankers understand the challenges small business owners face across different industries. We're here to help you build systems that work for your business.

Visit our Small Business Hub or stop by a branch to start a conversation about what's possible when cash flow works for you instead of against you.

Sources:

1 U.S. Chamber of Commerce, "Top Reasons Why Small Businesses Fail,"

https://www.uschamber.com/co/start/strategy/why-small-businesses-fail