- The 3x rule is outdated. Modern affordability depends on interest rates, regional costs, and your debt load, more than simple income multiples.

- Your debt matters as much as your salary. A $400/month car payment can reduce your home budget by $50,000 to $75,000.

- Interest rate shifts change everything. A 1% rate difference can alter your buying power by tens of thousands of dollars.

- Location reshapes the numbers. The same salary buys vastly different homes in Memphis versus Nashville versus Charleston.

- Dual income creates flexibility. Two $75,000 earners have different advantages than one $150,000 earner, particularly around job transitions and benefits.

Figuring out how much house you may afford on a $75,000 salary, $100,000 salary, or $150,000 salary isn't just about plugging numbers into a calculator and hoping for the best. It's about understanding what your income could realistically support when you factor in your debt, your savings, where you want to live, and what interest rates are doing right now. In 2025, home buying power by salary looks different than it did five years ago – and it looks different in Nashville than it does in Charleston or Memphis.

This guide walks through what mortgage affordability by income might look like at those common earning levels. We'll use scenario modeling to show you the range of possibilities, and we'll talk through the real-world factors that push those numbers up or down. Think of this as the context your calculator can't give you. Whether you're wondering how much mortgage you can afford with a $75,000 salary or exploring what a six-figure income unlocks, understanding mortgage affordability starts with seeing the full picture.

How to use this guide

This article uses scenario-based modeling with placeholder ranges to help you understand income-based mortgage affordability principles without making promises we can't keep. Your actual numbers will depend on your credit score, debt-to-income ratio, down payment amount, current interest rates, and the specific loan program you choose. The goal here isn't to tell you exactly what you'll qualify for. That's what pre-qualification with a mortgage loan originator is for. Instead, we're showing you how different factors interact and what questions you should be asking before you start house hunting. And, remember: if you're married or buying with a partner, lenders will look at combined income and combined debt. That changes everything.

The 3x income rule and why it doesn’t work anymore

You've probably heard the old guideline: buy a home that costs roughly three times your annual income. By that logic, someone earning $100,000 should target a $300,000 home. It's clean, it's simple, and it's outdated. That rule came from an era of lower home prices, lower interest rates, and more predictable property tax structures. Today, a buyer in one market might face annual property taxes of $2,500 on a home while a buyer in another market pays $8,000 on the same price. Insurance costs have climbed. HOA fees are more common. And interest rates, even when they're historically "normal," have a massive impact on what you can actually afford to pay each month. Modern affordability isn't about a multiplier. It's about whether your monthly housing payment might fit comfortably within your overall budget while leaving room for savings, retirement contributions, and everything else that makes life worth living. That's why lenders focus on debt-to-income ratios instead of simple salary multiples.

How debt shapes your buying power

Here's the truth that surprises first-time buyers: your student loans, car payment, and credit card balances matter just as much as your income when it comes to mortgage approval. Lenders calculate your debt-to-income ratio (DTI) by dividing your total monthly debt payments by your gross monthly income. Most conventional loans prefer to see a DTI below 43%, though some programs allow higher ratios with strong credit and reserves. Let's say you earn $75,000 a year. That's $6,250 per month before taxes. If you're already paying $800 for student loans and car payments, that leaves less room for a mortgage payment than someone earning the same salary with zero debt. This is why paying down high-interest debt before you apply for a mortgage could genuinely increase your buying power. It's not just about improving your credit score, though that helps too. It's about freeing up monthly cash flow that a lender may allocate toward your housing payment instead. The Consumer Financial Protection Bureau offers a detailed breakdown of how DTI works if you want to dig deeper into the mechanics.

How debt changes what you can afford (based on $100,000 salary):

| Debt level | Monthly debt | Home price range | Monthly payment | Buying power impact |

|---|---|---|---|---|

| No debt | $0 | $375,000 - $425,000 | $2,800 - $3,200 | Baseline |

| Moderate debt | $400 | $325,000 - $375,000 | $2,400 - $2,800 | -$50,000 to -$75,000 |

| Higher debt | $800 | $275,000 - $325,000 | $2,100 - $2,500 | -$100,000 to -$125,000 |

Assumes 6.5% rate, 10% down, 43% DTI cap. Payment includes principal, interest, taxes, insurance, and PMI.

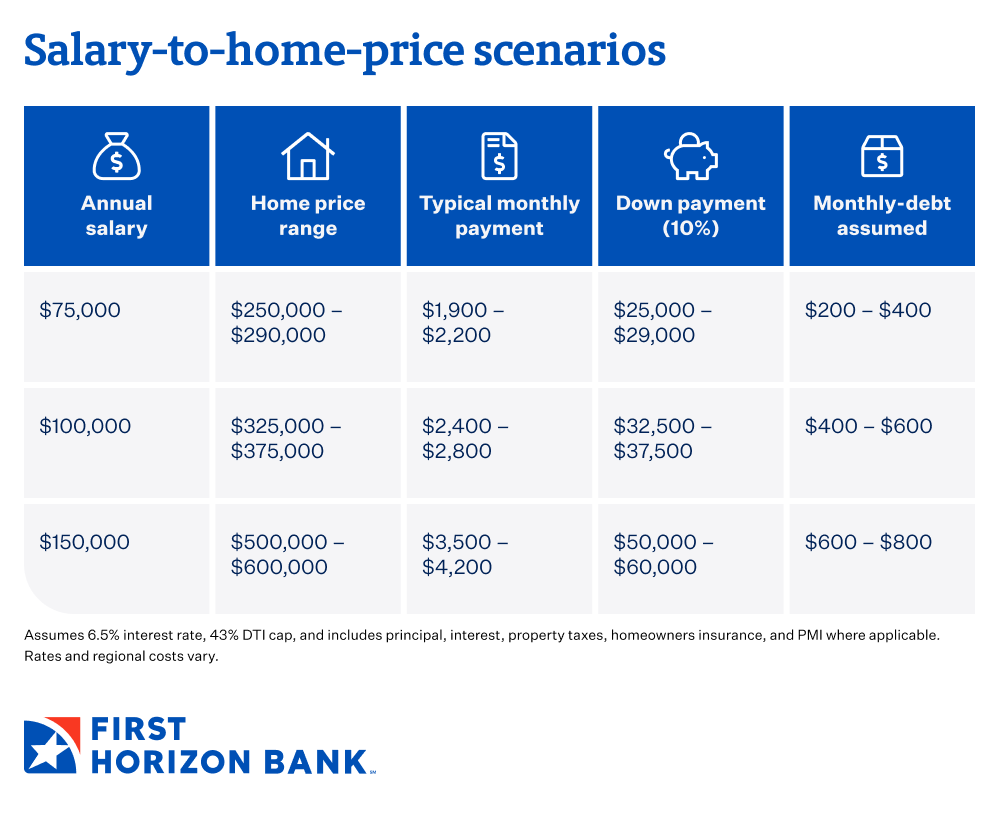

What you may afford on a $75,000 salary

A $75,000 salary puts you in a solid position for homeownership, especially if you're buying in a market with reasonable cost of living and you've kept your debt manageable. Let's model two scenarios. In the first, you're a single buyer with $400 in monthly debt payments (student loans and a car note). With a 10% down payment and current interest rates, you might comfortably afford a home in the $250,000 to $290,000 range, depending on property taxes and insurance in your area. Your monthly payment, including principal, interest, taxes, insurance, and private mortgage insurance, would likely land between $1,900 and $2,200.

Now let's change the variables. If you've paid down debt and you're entering the process with minimal monthly obligations, you might push into the low $300,000s even on a single $75,000 income. Or, if you're buying with a partner who also earns around $75,000, your combined household income opens up options we'll explore in the next section. The key is understanding that how much mortgage you can afford with a $75,000 salary isn't just about what you earn. It's about what you owe and what you've saved.

What you may afford on a $150,000 salary

A $150,000 salary gives you substantial flexibility in mortgage affordability, but it also comes with higher expectations around down payment, reserves, and financial planning. For a single buyer with minimal debt, you're likely looking at homes in the $500,000 to $600,000 range with a conventional loan and 15% to 20% down. Monthly payments could range from $3,500 to $4,200 depending on interest rates and regional costs.

If you're in a dual-income household with combined earnings of $200,000 or more, you're shopping in the $650,000 to $800,000 range in many markets. At this income level, discretionary spending becomes a bigger part of the conversation. Lenders will still approve you based on DTI, but you'll want to think carefully about how a $4,000 mortgage payment affects your ability to save for retirement, fund college accounts, or maintain the lifestyle you've built. This is also where regional variation really shows up. A $150,000 salary in a lower-cost market might mean a spacious new-construction home with acreage, but the same income in a high-demand urban market might mean a well-located townhome or condo. Neither is wrong. They're just different trade-offs based on what you value.

Dual-income advantage: understanding $75,000 + $75,000 vs. single $150,000

When two partners each earn $75,000, the combined $150,000 household income creates similar buying power to a single $150,000 earner, but with important differences. Dual-income households often have two sets of benefits (401k matching, health insurance options) and more financial flexibility if one partner changes jobs or takes parental leave. However, lenders will consider both partners' debts, so if one person carries significant student loans or credit card balances, it can offset the income advantage. The key is to calculate your combined DTI ratio before you start shopping.

How interest rates influence buying power

Interest rates are the invisible hand that shapes everything about affordability, and even small changes create big ripples. Let's use a simplified example. Imagine you're approved for a $350,000 mortgage. At a 6.5% interest rate, your monthly principal and interest payment would be around $2,212. If rates drop to 5.5%, that same loan amount costs you about $1,987 per month. That's a difference of $225 every month, or $2,700 per year. Over the life of a 30-year loan, that's more than $80,000 in savings. Now flip it the other way. If rates rise to 7.5%, your payment jumps to $2,448. Suddenly the home that felt affordable at 6.5% is stretching your budget. This is why timing matters, and it's also why working with a lender who understands rate locks, points, and refinancing strategies could be valuable. You might track current trends through resources like the Federal Reserve's 30-year mortgage rate data to get a sense of where the market is heading.

How regional factors reshape affordability

Where you buy matters just as much as how much you earn. Consider the Southeast. In Memphis, the median home price hovers around $220,000, property taxes are relatively low, and homeowners insurance is manageable.1 A buyer earning $100,000 might find a spacious single-family home in a good school district without stretching their budget. In Nashville, that same buyer is looking at a median price closer to $500,000, with higher property taxes and increased competition.2 In Charleston, waterfront proximity and tourism-driven demand push prices even higher, and flood insurance could add hundreds to your monthly payment.3 None of these markets is "better." They just require different strategies. If you're relocating for work or considering multiple cities, spend time researching not just home prices but also tax rates, insurance requirements, HOA prevalence, and commute costs.

Here's how five major Southeast markets compare on the key cost factors that shape affordability:

| Market | Median home price | Property tax rate | Annual insurance est. | Salary needed (single buyer)* |

|---|---|---|---|---|

| Memphis, TN | $220,000 | 1.52%7 | $1,800 | $65,000 - $75,000 |

| Knoxville, TN | $360,0005 6 | 0.83% | $1,700 | $90,000 - $105,000 |

| Charlotte, NC | $425,0004 | 0.92% | $1,900 | $105,000 - $120,000 |

| Nashville, TN | $500,000 | 0.95%8 | $2,100 | $120,000 - $135,000 |

| Charleston, SC | $550,000 | 0.57%** | $2,800*** | $135,000 - $150,000 |

*Salary needed assumes 10% down payment, 6.5% interest rate, 43% DTI cap, and moderate monthly debt ($400-$600).

**Charleston County effective rate; actual rates vary by municipality.

***Includes estimated flood insurance for coastal areas; properties outside flood zones may pay significantly less.

Data sources: Redfin, Realtor.com, local property assessor offices, Q4 2024 – Q1 2025. Home prices and insurance costs vary by neighborhood, property type, and specific location.

These numbers show why the same $100,000 salary creates vastly different buying power across the region. In Memphis, that income could comfortably support a $220,000 home with room in the budget for savings and lifestyle spending. In Charleston, the same salary might require stretching to afford a median-priced home, or choosing a property outside the most expensive coastal areas. Understanding these regional differences is essential for setting realistic expectations and making informed decisions about where to buy. The HUD Comprehensive Housing Affordability Strategy data could help you compare cost of living and housing affordability across regions.

Preparing for your down payment

Your down payment is the key that unlocks the door. The more you put down, the lower your monthly payment, the less interest you'll pay over time, and the sooner you'll build equity. Conventional loans (backed by Fannie Mae or Freddie Mac) typically require at least 5% down and offer the most flexibility for repeat buyers. The catch? If you put down less than 20%, you'll pay private mortgage insurance until you reach that equity threshold. FHA loans allow as little as 3.5% down, making them popular with first-time buyers, but they require both upfront and monthly mortgage insurance. VA loans, available to eligible veterans and service members, offer 0% down with no PMI. That's often the best deal available if you qualify. Your mortgage loan originator may help you compare which program gives you the best combination of down payment requirements, interest rates, and monthly costs.

Let's say you're targeting a $300,000 home with 10% down. You need $30,000 plus $6,000 to $9,000 for closing costs. That's roughly $36,000 to $39,000 total. Here's what that looks like at different monthly savings rates: $500/month gets you there in 6 years, $750/month takes 4 years, and $1,000/month means 3 years. If that timeline feels long, consider these accelerators: tax refunds, work bonuses, side income, or gift funds from family (which many loan programs allow). The faster you save, the sooner you build equity instead of paying rent. First Horizon's Automatic Savings Service could help you build that fund without thinking about it.

Ready to see your real numbers?

The scenarios we've walked through here are starting points, not guarantees. Your actual buying power depends on your unique financial profile: your credit history, your debt load, your savings, the loan programs you qualify for, and the market where you're buying. The best next step is to get pre-qualified so you know exactly where you stand before you start touring homes. Pre-qualification gives you clarity, confidence, and credibility with sellers. It helps you avoid the heartbreak of falling in love with a home that's out of reach. Ready to move forward? Use our home affordability calculator to estimate your buying power, explore mortgage loan options that fit your goals, or connect with a local mortgage expert who can give you personalized guidance. Homeownership is one of the biggest financial decisions you'll make. Let's make sure you're walking into it with your eyes wide open and a plan that actually works.

Frequently asked questions

How much house could I afford with a $75,000 salary?

With a $75,000 annual income, you may typically afford a home in the $250,000 to $290,000 range if you have manageable debt and a down payment of 10% or more. Your exact range depends on your debt-to-income ratio, credit score, and local property taxes and insurance costs.

What salary do I need to buy a $400,000 house?

To comfortably afford a $400,000 home, you would generally need a household income of at least $100,000 to $120,000, assuming you have minimal debt, a down payment of 10% to 15%, and current interest rates. Lenders typically want your total monthly debt payments to stay below 43% of your gross income.

Does my debt affect how much mortgage I might get?

Yes, substantially. Lenders calculate your debt-to-income ratio by dividing your monthly debt payments (student loans, car loans, credit cards) by your gross monthly income. Higher debt reduces the amount you may be able to borrow because it limits how much of your income could go toward a mortgage payment.

How do interest rates change what I might afford?

Interest rates directly impact your monthly payment and total buying power. A 1% increase in rates could reduce your buying power by 10% or more, and a 1% decrease might increase it by a similar margin. Even small rate changes create substantial differences over a 30-year loan.

Should I wait to buy until I have 20% down?

Not necessarily. Many buyers successfully purchase homes with 5% to 10% down using conventional or FHA loans. The key is understanding the trade-offs (you'll pay PMI with less than 20% down) and ensuring your monthly payment still fits your budget comfortably.

How does location affect affordability?

Location impacts property taxes, homeowners insurance, HOA fees, and median home prices. A $100,000 salary might buy you a spacious home in a lower-cost market but only a modest townhome in a high-demand city. Regional cost differences could shift your buying power by $100,000 or more.

Sources:

1 Memphis Area Association of Realtors, "Area home sales increased 13% compared to 2024,"

https://www.maar.org/news/2025/10/13/homepage/area-home-sales-increased-13-compared-to-2024

2 Greater Nashville Realtors, "2024 Housing Market Highlights,"

https://www.greaternashvillerealtors.org/news/2025/01/12/real-deal-column/2024-housing-market-highlights/

3 Realtor.com, "Charleston, SC 2025 Housing Market,"

https://www.businesswire.com/news/home/20250708925398/en/Gen-X-Prioritises-Security-Over-Convenience-in-Payment-Choices-PXP-Report-Finds

4 Redfin, "Charlotte, NC Housing Market,"

https://www.redfin.com/city/3105/NC/Charlotte/housing-market

5 Realtor.com, "Knoxville, TN 2025 Housing Market."

https://www.realtor.com/realestateandhomes-search/Knoxville_TN/overview

6 Redfin, "Knoxville, TN Housing Market,"

https://www.redfin.com/city/10200/TN/Knoxville/housing-market

7 Ownwell, "Memphis, Shelby County, Tennessee Property Taxes,"

https://www.pewresearch.org/internet/2017/05/17/tech-adoption-climbs-among-older-adults/

8 Ownwell, "Nashville, Davidson County, Tennessee Property Taxes,"

https://www.ownwell.com/trends/tennessee/davidson-county/nashville