- The 1% Rule: A 1% interest rate increase reduces your purchasing power by approximately 10%, potentially cutting $40,000 from your budget on a $400,000 loan.

- Rate Locks Provide Protection: Lock your rate during the shopping phase to protect your budget from market volatility while you search for the right home.

- Date the Rate, Marry the House: Buy a home you can comfortably afford today, then refinance later if rates drop, but only if the numbers work without counting on future savings.

- Strategy Over Speculation: The right home at a rate you can afford beats waiting for the perfect rate in the wrong home, or no home at all.

You're pre-qualified. You've got your budget. You're ready to start looking at homes. Then you check the news and see mortgage rates jumped again overnight. Suddenly, you're wondering if the $450,000 home you could afford last month is now out of reach.

You're not imagining things. Since 2021, a 3% rate increase has reduced the average buyer's purchasing power by approximately $150,000. That's not a typo. Rate volatility doesn't just affect your monthly payment.5 It reshapes your entire budget, sometimes in a matter of weeks.

Here's what most buyers don't realize: you have more control than you think. The question isn't "What's your rate today?" The real question is "How do we protect your buying power?" In this article, you'll learn three strategic frameworks that shift you from reactive anxiety to proactive strategy: the 1% Rule that quantifies exactly how rate changes impact your budget, rate locks that protect your purchasing power while you shop, and a balanced perspective on the "Date the Rate, Marry the House" philosophy. Your First Horizon Loan Officer isn't just watching rates. They're watching out for you.

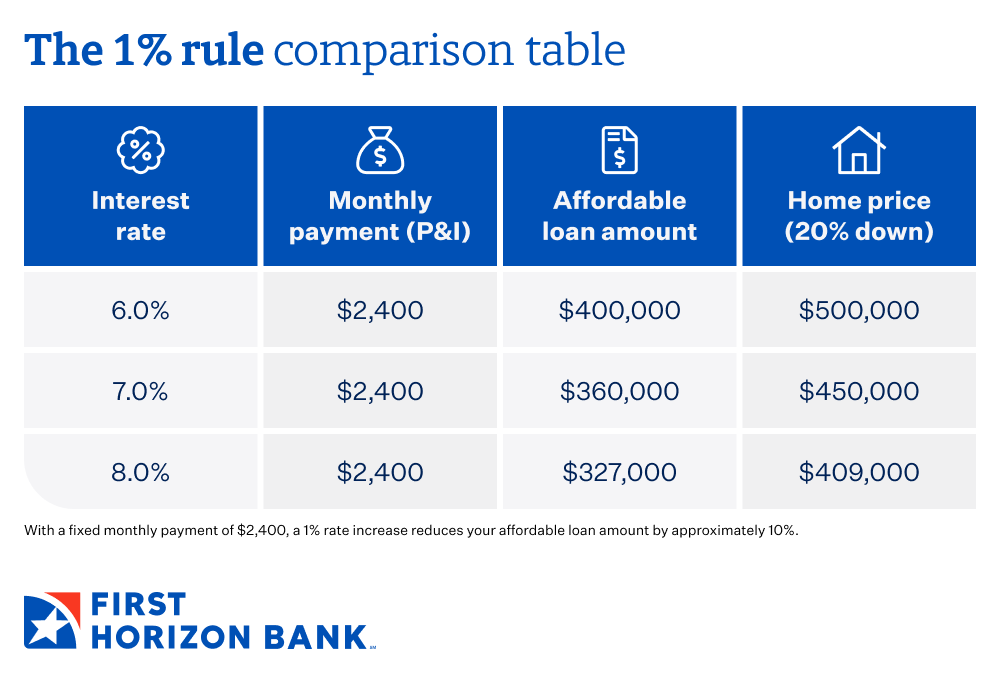

How a 1% rate change impacts your buying power

Let's start with the math that matters. The 1% Rule states that a 1% interest rate increase reduces your purchasing power by approximately 10%. Understanding how interest rates affect affordability isn't meant to create anxiety, it's about making informed decisions.3

Here's a real-world example. Let's say you're comfortable with a $2,400 monthly mortgage payment for principal and interest. At a 6% interest rate, that payment qualifies you for a $400,000 loan. Put 20% down, and you're shopping for homes around $500,000. Now, rates increase to 7%. That same $2,400 monthly payment now only qualifies you for a $360,000 loan, which is $40,000 less in purchasing power. Your home shopping budget just dropped from $500,000 to $450,000. At 8%, you're down to a $327,000 loan and a $409,000 home price. Same monthly payment, $91,000 less buying power.

This happens because your interest rate directly affects how much of your monthly payment goes to principal versus interest. Even a small rate change compounds over 30 years. During the 2021-2025 rate environment, buyers watched their purchasing power shrink as rates climbed from historic lows near 3% to peaks above 7%1. Current mortgage rate trends continue to show volatility in today's market.2 When you know exactly how rate changes affect your budget, you can plan strategically instead of reacting emotionally. You can use tools like the First Horizon Mortgage Calculator to see the rate impact on your specific budget and make decisions based on real numbers, not headlines.

How rate locks protect your buying power while you shop

Now that you understand how rate volatility affects your budget, let's talk about protection. A rate lock is a guarantee that your interest rate won't increase during a specified period, typically while you're shopping for a home and closing on your purchase. Think of it as insurance for your purchasing power.

Here's how it works in practice. After you're pre-qualified, you lock your rate with your lender. This "lock and shop" approach lets you search for homes knowing your exact budget won't shrink if rates increase next week. You find the right home, make an offer, and close within your lock period without rate risk. If rates jump during that time, you're protected. Your budget stays intact.

Rate lock terms vary by lender and region. When discussing rate locks with your First Horizon Loan Officer, ask about:

- Available lock periods and which timeline fits your situation

- Any costs or fees associated with locking or extending

- Whether float-down options are available if rates decrease

- How the lock process works from application to closing

Your loan officer can explain the specific options available in your area and help you choose the right strategy for your timeline. Rate locks provide confidence to make decisions. When you know your budget is secure, you can evaluate homes based on fit and value, not fear. You're shopping with certainty in an uncertain market.

Should you buy now or wait for rates to drop?

This is the question every buyer asks right now. The answer isn't simple, but there's a framework that helps: "Date the Rate, Marry the House." The idea is straightforward. Buy the right home at today's rates, then refinance later if rates drop. But like any strategy, it works brilliantly in some situations and backfires in others.

When it works

Sarah and Tom found a home they love at $450,000. At today's 7% rate, their monthly payment is $2,661, well within their budget at 28% of their gross income. They plan to stay for at least 10 years, and the home meets their long-term needs: good schools, space for a growing family, reasonable commute. Even if rates never drop, they're comfortable with this payment. If rates do fall to 6% in two years, they can refinance and save $198 per month.4 Nice bonus, but not required for their financial stability. This is "dating the rate" done right.

The strategy works when you can comfortably afford the home at current rates, plan to stay 5+ years so transaction costs make sense, and the home genuinely meets your long-term needs regardless of rate changes.

When to be cautious

Mike is stretching to afford a $500,000 home at 7%, with a monthly payment of $2,995. That's 35% of his gross income, above the comfortable 28-30% range most financial advisors recommend. He's counting on refinancing in 18 months when rates "should" drop to 6%, which would bring his payment to $2,698, still tight, but more manageable. This is risky. He's betting on a future that's uncertain and overextending his budget today.

Be cautious if you're overextending your budget, planning short-term ownership, or facing income uncertainty. If you can barely afford the house, you're not dating the rate. You're gambling on it.

What happens if rates drop after I lock?

Some lenders offer float-down options that allow you to capture a lower rate if rates drop significantly (typically 0.25%+ decrease), though fees or restrictions may apply. Your First Horizon Loan Officer can explain what options are available based on your loan type and timeline. Remember that a rate lock's primary value is protection from increases. If rates drop slightly, the certainty and protection of your lock often outweigh a small potential savings.

Is it better to wait for rates to drop?

No one can predict when or if rates will drop. Waiting means you might miss the right home or face increased competition when rates fall. A better approach is to buy a home you can comfortably afford at today's rates. If rates drop later, you can refinance. If they don't, you're still in a home that works for you. The right home at a rate you can afford beats the perfect rate in the wrong home. Focus on what you can control: your budget, your timeline, and finding a home that meets your needs.

Buy with confidence, not anxiety

Rate volatility is real, but it doesn't have to derail your homeownership plans. The difference between anxious buyers and confident buyers isn't luck: it's strategy. Now, you have three frameworks that shift you from reactive to proactive: the 1% Rule helps you understand exactly how rate changes impact your budget, rate locks protect your purchasing power during the shopping phase, and the "date the rate" philosophy guides your timing decisions with clear criteria instead of speculation.

Buying power protection starts with the right partner. Your First Horizon Loan Officer doesn’t just provide rate quotes. They're Market Watchers who help you navigate uncertainty with strategy and protection.

Rate volatility is a reality, but with the right strategy and partner, it doesn't have to stop you from finding the home where your next chapter begins.

Ready to explore your purchasing power?

Connect with a First Horizon Loan Officer to discuss your options and protect your budget in today's market.

Sources:

1 Federal Reserve Economic Data (FRED), "30-Year Fixed Rate Mortgage Average,"

https://fred.stlouisfed.org/series/MORTGAGE30US

2 Freddie Mac, "Primary Mortgage Market Survey,"

https://www.freddiemac.com/pmms

3 Consumer Financial Protection Bureau, "Owning a Home: Mortgage Estimate,"

https://www.consumerfinance.gov/owning-a-home/mortgage-estimate/

4 Bankrate, "Mortgage Refinancing Guide,"

https://www.bankrate.com/mortgages/refinancing/

5 National Association of Realtors, "Research and Statistics,"

https://www.nar.realtor/research-and-statistics