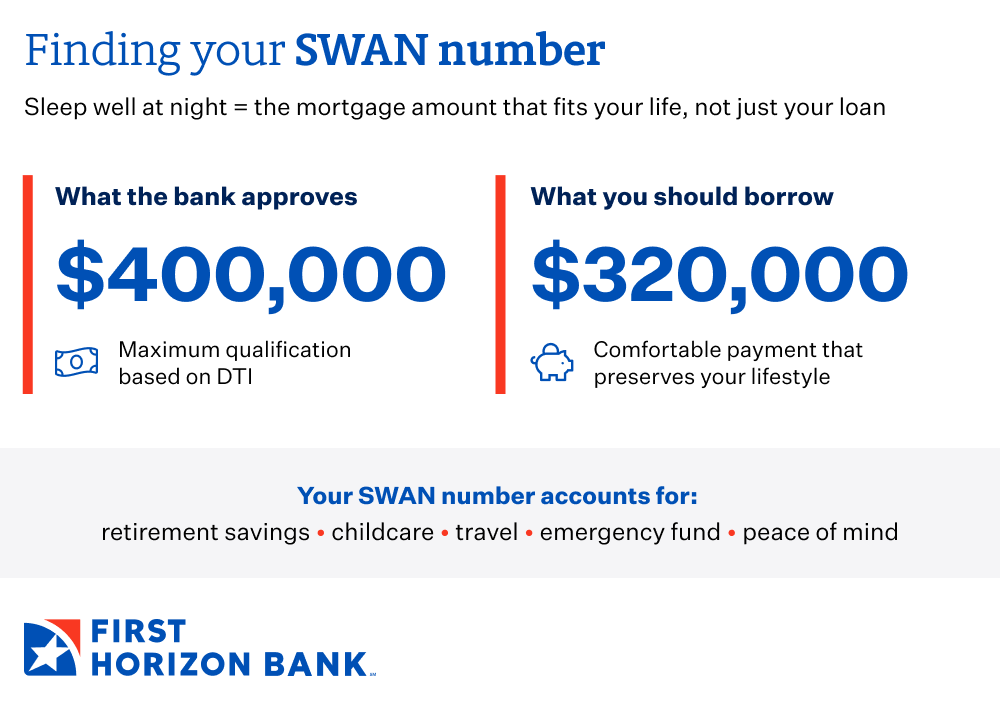

- Your pre-approval amount represents the maximum a lender will risk, not necessarily what fits your life comfortably.

- The 28% rule offers a conservative starting point: keep your mortgage payment at or below 28% of your gross monthly income.

- True homeownership costs extend beyond your mortgage payment to include property taxes, insurance, maintenance, and unexpected repairs.

- A personal lifestyle audit reveals your real affordability by accounting for retirement savings, childcare, travel, and the financial cushion you need for peace of mind.

- Your banker should be a strategic partner who helps you find your "SWAN number"—the mortgage amount that lets you Sleep Well At Night.

You open the email from your lender, and there it is: your pre-approval letter. The number is bigger than you expected. For a moment, you imagine the extra bedroom, the finished basement, the neighborhood with the better schools. Then, quietly, a question surfaces: "But could we really afford that?"

That hesitation? It's not doubt. It's wisdom.

Here's the truth most first-time homebuyers discover too late: just because you could eat the whole pizza doesn't mean you should. The same applies to mortgages. The amount you qualify for and the amount you should actually borrow are often two very different numbers.

At First Horizon, we believe your home should bring you confidence, not anxiety. That's why we talk about finding your SWAN number (the mortgage amount that lets you Sleep Well At Night). Not the maximum you might technically qualify for on paper, but the payment that fits comfortably within your real life, with all its complexity, goals, and unexpected moments.

This article will walk you through how to find that number for yourself.

What your pre-approval number really means

When a lender pre-approves you for a mortgage, they're making a calculated assessment of risk. They look at your income, your existing debts, and they run a formula called your debt-to-income ratio (DTI)1.

Most conventional lenders will approve borrowers with a DTI up to 43%, though some programs allow even higher ratios. What does that mean in practice? If you earn $6,000 per month before taxes, a lender might approve you for total monthly debt payments (including your new mortgage, car loans, student loans, and credit cards) of up to $2,580.

Here's what's important to understand: that DTI threshold represents the maximum risk the bank is willing to take. It's not a recommendation. It's not financial advice tailored to your life. It's a standardized metric designed to protect the lender's investment.

The bank's calculation doesn't know that you're planning to start a family next year. It doesn't account for the fact that you value having a robust emergency fund, or that you're committed to contributing 15% of your income to retirement. It doesn't factor in that your aging car will need replacing soon, or that your industry experiences seasonal income fluctuations.

Your pre-approval number is the ceiling. Your job is to find your floor: the foundation of what actually works for your life.

The 3x income rule and why it doesn’t work anymore

You've probably heard the old guideline: buy a home that costs roughly three times your annual income. By that logic, someone earning $100,000 should target a $300,000 home. It's clean, it's simple, and it's outdated. That rule came from an era of lower home prices, lower interest rates, and more predictable property tax structures. Today, a buyer in one market might face annual property taxes of $2,500 on a home while a buyer in another market pays $8,000 on the same price. Insurance costs have climbed. HOA fees are more common. And interest rates, even when they're historically "normal," have a massive impact on what you can actually afford to pay each month. Modern affordability isn't about a multiplier. It's about whether your monthly housing payment might fit comfortably within your overall budget while leaving room for savings, retirement contributions, and everything else that makes life worth living. That's why lenders focus on debt-to-income ratios instead of simple salary multiples.

A simple starting point: the 28% rule

If you're looking for a practical guardrail, the 28% rule offers a sensible place to begin. This guideline suggests keeping your total housing payment at or below 28% of your gross monthly income.

Let's make this concrete. Say you earn $75,000 annually, which translates to $6,250 per month before taxes. Twenty-eight percent of that monthly income equals $1,750. That's your target maximum for your total monthly housing payment, including principal, interest, property taxes, and homeowners insurance.

Here's how that might break down:

Monthly payment breakdown:

Principal and interest = $1,200

Property taxes = $350

Homeowners insurance = $200

Your total monthly payment = $1,750

At a 7% interest rate, that $1,200 in principal and interest would support roughly a $180,000 mortgage. Add a 20% down payment of $45,000, and you're looking at a $225,000 home purchase price.

Your monthly mortgage statement shows principal and interest. But homeownership demands much more. Understanding PITI (principal, interest, taxes, and insurance) is just the beginning.

Property taxes vary dramatically by location. In some areas, annual property taxes run less than 0.5% of your home's value. In others, they exceed 2%. A $300,000 home in a high-tax area could cost you $6,000 annually in property taxes alone. That's $500 per month that doesn't build equity.

Homeowners insurance protects your investment, but premiums have climbed significantly in recent years, particularly in regions prone to natural disasters. Budget $100 to $300 monthly, depending on your home's value and location.

HOA fees, if applicable, often range from modest to substantial. That $400 monthly HOA fee in a condo community adds nearly $5,000 to your annual housing costs.

Then there's maintenance and repairs. The general rule of thumb is to budget 1-2% of your home's purchase price annually for upkeep. For a $300,000 home, that's $3,000 to $6,000 per year, or $250 to $500 monthly. New roof. Failed water heater. HVAC repair. Foundation issues. These aren't possibilities – they're inevitabilities. Understanding these major home maintenance costs helps you budget realistically from the start.3

Rising homeownership costs have outpaced income growth in many markets, making this comprehensive view of affordability more critical than ever.2 When you calculate what you might truly afford, you need to see the complete picture, not just the mortgage payment.

The lifestyle audit: a checklist for your real-life budget

Numbers on a spreadsheet tell part of the story. Your life tells the rest.

Before you commit to a mortgage payment, conduct an honest lifestyle audit. This isn't about judgment or sacrifice. It's about clarity. You're designing a financial life that supports what matters most to you.

Start with retirement. How much are you currently saving, and how much should you be saving? If you're 30 years old and want to retire comfortably, financial advisors typically recommend saving 15% of your gross income. If you're earning $75,000 annually, that's $11,250 per year, or roughly $940 per month. Will your budget allow you to maintain that contribution with your proposed mortgage payment?

Consider childcare costs. If you have young children or plan to start a family, childcare represents one of the largest line items in many household budgets. Depending on your location, full-time daycare for one child often costs $1,000 to $2,000 monthly. Two children? Double it.

Account for transportation. What are your car payments? How much do you spend on gas, insurance, and maintenance? If you're buying in a location that requires longer commutes, those costs increase. If your current vehicle has 150,000 miles on it, you'll likely need to replace it within your mortgage term.

Evaluate your lifestyle priorities. Do you travel annually? That matters. Do you have hobbies that require investment, whether that's golf, skiing, photography, or music? Include them. Are you supporting aging parents or contributing to a child's college fund? Factor it in.

Build in margin for the unexpected. Medical expenses. Veterinary emergencies. Job transitions. Life happens, and margin in your budget is what allows you to handle it without panic.

This audit isn't about talking yourself out of homeownership. It's about talking yourself into the right amount of homeownership (the amount that coexists peacefully with everything else you value.)

Beyond the mortgage: the total cost of homeownership

One of the fastest ways to become house poor is to focus exclusively on whether you might make the mortgage payment while ignoring everything else that comes with owning a home.4

Your monthly mortgage statement shows principal and interest. But homeownership demands much more. Understanding PITI (principal, interest, taxes, and insurance) is just the beginning.

Property taxes vary dramatically by location. In some areas, annual property taxes run less than 0.5% of your home's value. In others, they exceed 2%. A $300,000 home in a high-tax area could cost you $6,000 annually in property taxes alone. That's $500 per month that doesn't build equity.

Homeowners insurance protects your investment, but premiums have climbed significantly in recent years, particularly in regions prone to natural disasters. Budget $100 to $300 monthly, depending on your home's value and location.

HOA fees, if applicable, often range from modest to substantial. That $400 monthly HOA fee in a condo community adds nearly $5,000 to your annual housing costs.

Then there's maintenance and repairs. The general rule of thumb is to budget 1-2% of your home's purchase price annually for upkeep. For a $300,000 home, that's $3,000 to $6,000 per year, or $250 to $500 monthly. New roof. Failed water heater. HVAC repair. Foundation issues. These aren't possibilities — they're inevitabilities. Understanding these major home maintenance costs helps you budget realistically from the start.

Rising homeownership costs have outpaced income growth in many markets, making this comprehensive view of affordability more critical than ever. When you calculate what you might truly afford, you need to see the complete picture, not just the mortgage payment.

Why your banker is your best partner

Here's what separates a transaction from a partnership: a good banker's job isn't to sell you the biggest loan you qualify for. It's to help you make the most informed decision for your unique situation.

When you sit down with a First Horizon banker, you're not just discussing loan products and interest rates. You're having a conversation about your life. Where do you see yourself in five years? What are your career plans? Are you planning to grow your family? What does financial security mean to you?

A banker who takes time to understand your complete picture may help you stress-test different scenarios. What happens to your budget if interest rates are slightly higher when you buy? What if one spouse takes parental leave? What if you decide to pursue a career change that involves a temporary income reduction?

Your banker is also the right person to introduce you to First Horizon's mortgage affordability calculator, which allows you to model different purchase prices, down payments, and interest rates to see how they affect your monthly payment.

This collaborative approach means you're not left alone with a pre-approval letter and a stack of online listings, wondering which homes are truly within reach. Instead, you have a knowledgeable partner who walks you through the numbers, explains the tradeoffs, and helps you find your SWAN number.

The right banker celebrates with you when you find a home you love and could genuinely afford, not when you stretch to the absolute maximum of your approval.

Frequently asked questions

What is a good rule of thumb for mortgage affordability?

The 28% rule is a reliable starting point: keep your total monthly housing payment at or below 28% of your gross monthly income. This guideline typically leaves room in your budget for other financial priorities, like retirement savings, emergency funds, and lifestyle expenses. However, your personal comfort zone may be lower depending on your complete financial picture and goals.

Does pre-approval mean I could afford that amount?

Not necessarily. Pre-approval indicates the maximum amount a lender is willing to risk based on your income and debt-to-income ratio. It doesn't account for your personal financial goals, lifestyle expenses, savings priorities, or the peace of mind you need. Your actual affordability should factor in all the costs of homeownership plus your unique budget requirements.

What does it mean to be house poor?

Being house poor means spending such a large percentage of your income on housing costs that you have little left for other expenses, savings, or financial goals. People who are house poor may struggle to afford basic necessities, experience difficulty saving for emergencies or retirement, and feel constant financial stress despite owning a home. It happens when buyers focus only on qualifying for a mortgage rather than determining true affordability.

What is PITI?

PITI stands for Principal, Interest, Taxes, and Insurance. It represents the four main components of your total monthly mortgage payment. While your principal and interest are paid to your lender, the taxes and insurance portions are often collected by the lender and held in an escrow account to be paid on your behalf. Understanding your full PITI payment is essential for determining true affordability.

How much should I budget for home maintenance and repairs?

Financial experts recommend budgeting 1-2% of your home's purchase price annually for maintenance and repairs. For a $300,000 home, that's $3,000 to $6,000 per year, or roughly $250 to $500 monthly. Newer homes may require less initially, while older homes often need more. Major home maintenance costs like roof replacement, HVAC systems, and foundation repairs often run into thousands of dollars.

Should I max out my pre-approval amount to get more house?

Only if it genuinely fits your complete financial picture. A larger home comes with higher costs beyond the mortgage (more to heat and cool, more to maintain, higher property taxes, and more expensive repairs). Many homeowners find greater financial peace and flexibility by purchasing below their maximum approval, leaving room in their budget for savings, lifestyle priorities, and unexpected expenses.

Buying a home that brings you confidence

Homeownership should feel like freedom, not a financial trap. It should open up possibilities in your life, not close them down.

Your SWAN number (your Sleep Well At Night mortgage amount) comes from three steps. First, use the 28% rule as your conservative starting point. Second, calculate the total costs of homeownership, including taxes, insurance, maintenance, and all those expenses that don't show up in your mortgage payment. Third, conduct an honest lifestyle audit that accounts for your retirement savings, family plans, career goals, and the financial margin you need to handle life's surprises.

The most important step? Talk to a banker who performs their role as your partner, not your salesperson.

At First Horizon, we've built our reputation on relationships that last well beyond closing day. We want you in a home that fits your life today and grows with you into the future. We want you to feel confident in your decision, not anxious about your payment.

Your home should be your foundation, not your burden.

Find your SWAN number.

Connect with a First Horizon banker who walks you through your budget, lifestyle goals, and mortgage options. Together, we'll help you build a mortgage plan that fits your life, not just your loan. For more guidance on your homebuying journey, you may also explore our Personal Learning Center's home buying resources, where you'll find comprehensive information on every stage of the process. If you'd like to begin exploring numbers on your own, our mortgage affordability calculator allows you to model different scenarios based on your income and goals.

Sources:

1 Consumer Financial Protection Bureau, "What is a debt-to-income ratio?"

https://www.consumerfinance.gov/ask-cfpb/what-is-a-debt-to-income-ratio-en-1791

2 Harvard Joint Center for Housing Studies, "The Rising Costs of Homeownership,"

https://www.jchs.harvard.edu/blog/rising-costs-homeownership-are-increasing-burdens

3 Bankrate, "What Are the Most Expensive Home Maintenance Costs?"

https://www.bankrate.com/home-equity/most-expensive-home-maintenance-costs

4 Investopedia, "House Poor Definition,"

https://www.investopedia.com/terms/h/housepoor.asp